We roasted through a hot weekend but have been blessed with a comparatively cool spring and we expect cooler than normal temperatures over the next several days. That’s great news since we aren’t feeling the extreme temperatures…at least not yet. Bring em’ on in July, but let’s keep them at bay in June (as if we have any control over such things…those of you controlling the weather, little help?).

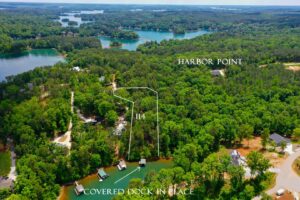

We were able to close on a Lake Keowee area home, as well as put some Lake Keowee area acreage under contract over the past week and we listed a Clemson condo. Buyer activity remains strong as properties continue to go under contract. Also, we are seeing an increase in inventory that’s outpacing the buyers by a bit. That’s to be expected this time of year as folks put their Lake Keowee properties on the market when the buyers are out in force. The number of buyers in the market will continue to increase until it hits a high point around mid-July.

That’s why if you’ve been considering putting your Lake Keowee real estate on the market, now is a crucial time! Let’s meet and discuss where you stand, what needs to be addressed and what your best move forward would be.

Summer has just started but there is time to find that perfect Lake Keowee real estate or sell your current Lake Keowee real estate to buy another. We’re here to help! [email protected][email protected] 864-270-9186.

A Critical Guide to Home Loans:

Your Options And How They Affect Your Future

Choosing the right mortgage will affect your very financial future. Here’s vital information to help you weigh your options and make a sound decision.

An Insider’s Guide to Understanding Mortgage Loans

Shopping for a mortgage lender

there are several potential lenders in today’s marketplace. They include:

Mortgage Banks – A mortgage banker is a direct lender. He or she qualifies applicants, finds the best available loan and funds it. Because this is their main business, mortgage banks can offer very competitive rates – but are not necessarily the cheapest.

Mortgage Brokers – Brokers don’t lend money; they find lenders for a fee in addition to the traditional application and processing costs. While a good broker might be able to find you the cheapest mortgage, maker sue the fee doesn’t offset any savings. Since most brokers’ fees are paid by the lender in the form of a commission, their services cost you nothing – that is, no out-of-pocket costs. Something also to remember – a mortgage broker is the legal agent of his or her client and does not work for the lending institution. So, a mortgage broker will have access to the widest spectrum loan options – whereas a bank or savings and loan representative will draw from only “in-house” loan options. Going by this information, a reputable mortgage broker would most likely be your cheapest source for home loans and refinancing.

Savings and Loan – Once the primary source of home financing, savings and loans hold a much smaller piece of the market today. But some experts recommend checking their offers before looking at a bank.